- 2411

- 0

Sharing Ideas and Updates on LPG in Nigeria and related information to enable effective collaboration within the LPG Value Chain

Is The Nigerian LPG Market Saturated? Navigating A Crowded Industry.

Is The Nigerian LPG Market Saturated? Navigating A Crowded Industry.

For the LPG Day on the 7th of June, 2025, we decided to open our platforms and groups to the general public as we often do. Now the result of this was an enlightening conversation on the industry at large and among one of the standout conversation was the topic of over saturation within this industry. So let’s explore together.

The Nigerian Liquefied Petroleum Gas (LPG) industry, once regarded as a promising frontier for clean energy and small business investment, is increasingly being viewed through a different lens—one of intense saturation, thinning margins, and uncertainty. As one LPG business owner lamented in a recent WhatsApp discussion:

“Everyone is now selling LPG—both licensed and unlicensed. It’s terrible.”

From Blue Ocean to Red Ocean

In the early 2010s, LPG plants in Nigeria enjoyed robust profits, spurred by government efforts to deepen gas penetration and reduce reliance on firewood. But in 2025, the picture has changed. Multiple factors have contributed to what many now call a “crowded marketplace.”

Ease of Entry: The relative simplicity of establishing a skid plant or mobile refilling unit has led to a proliferation of both licensed and unlicensed operators.

Regulatory Lapses: Weak enforcement by the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) has enabled widespread non-compliance. "Just buy a tank and start selling" has become an unfortunate norm.

Urban Clustering: Most new entrants are setting up shop in already-congested urban or semi-urban areas, leading to cannibalization of market share.

The Price War and Vanishing Margins

As competition intensifies, the first casualty is often pricing. LPG retailers are now locked in a race to the bottom—undercutting each other in a bid to attract customers.

“You’ll buy a product today, and before you finish selling it, the price has dropped or increased. It’s hard to make a profit,” another operator said.

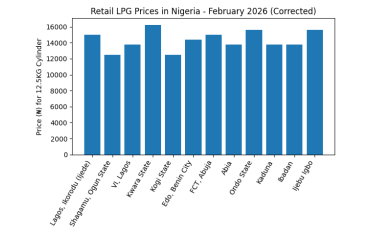

According to recent market surveys, profit margins can shrink to as low as ₦50 per kilogram in some urban centers—barely enough to cover running costs like diesel, staff salaries, equipment maintenance, and rent. Business owners reported selling 10 tonnes of LPG in 6 weeks and barely breaking even.

Location, Scale, and Strategy: The New Currency

In today’s LPG market, success is increasingly tied to strategic factors beyond just owning a gas plant:

Location is Everything: Operators who set up shop in under-served or peri-urban communities report better sales volume and customer loyalty. Densely populated residential areas with poor access to major stations remain lucrative.

Economies of Scale: Plants with 10- or 20-tonne capacities enjoy better supplier terms and logistics efficiency, giving them an edge over smaller 2–5-tonne plants.

Value-Added Services: Forward-thinking businesses are differentiating themselves through:

Home delivery and online ordering

Flexible refill options (pay-per-use, loyalty discounts)

Community engagement and education on safe gas usage

Extended operation hours to serve night users

Solutions: How Can Stakeholders Navigate This Crisis?

While the current conditions are challenging, all hope is not lost. Here are a few steps that can make a difference:

Policy Reform: Stronger enforcement from the NMDPRA and local governments is urgently needed to clamp down on illegal operations and standardize safety practices.

Industry Data: There’s a lack of reliable, real-time market data on LPG demand, pricing, and consumer behavior. Better data will aid forecasting and planning.

Collaboration over Competition: Rather than viewing other plant owners as threats, local LPG operators should explore shared services, joint procurement, and community-based unions—not to fix prices but to enhance resilience.

Diversification: Business owners can pivot into complementary LPG services like cylinder sales, accessories, CNG conversions, and training services.

Conclusion: A Market in Transition, Not Collapse

The Nigerian LPG market is not necessarily saturated—it’s evolving. The entry of new players, while threatening to existing ones, also reflects growing national adoption of clean cooking fuels. Rather than retreating, stakeholders must adapt, innovate, and demand better governance of the sector.

The words of one long-time operator sum it up well:

“It’s a free market, but only those with strategy will survive.”

Share on Social Media:

Are you setting up, or do you need LPG information? Get started with our LPG and CNG Webinars!

Do you need LPG Depot Prices and Mont Belvieu Prices Data Sheet (2019 till date)? Get Access here!

You May Also Like

0 Comment.